TL;DR:

- Big Lots' bankruptcy transformed its stock into a risky OTC security governed by court proceedings and claim seniority. Investors must recognize that post-bankruptcy securities like BIGGQ are driven by restructuring outcomes rather than operational performance. Understanding claim hierarchy and legal processes is essential before trading or investing in such distressed equities.

Most investors still search for Big Lots stock expecting a beaten-down retail play with recovery potential. What they find instead is fundamentally different: a bankruptcy security trading under the ticker BIGGQ, governed not by earnings multiples or revenue trends but by court proceedings, claim seniority, and restructuring outcomes. The gap between what investors expect and what they actually hold is wide, and that gap is costly.

Key Takeaways

| Point | Details |

|---|---|

| Bankruptcy changes everything | Big Lots’ 2024 bankruptcy turned its shares into a special security where restructuring, not business results, drives value. |

| Standard analysis doesn’t apply | Valuation now depends on bankruptcy process outcomes, not normal financial metrics. |

| Risks are higher for investors | Shareholders may be wiped out or receive little value depending on recovery terms and claim seniority. |

| Comparison is crucial | Studying other bankrupt stocks can reveal patterns and pitfalls when considering post-bankruptcy investments. |

| Use specialized tools | Advanced analysis and risk calculators help investors make informed choices about distressed and bankruptcy securities. |

How Big Lots' bankruptcy reshaped its stock

Big Lots was once a recognizable American discount retailer with hundreds of stores and a Nasdaq-listed stock. That reality changed when Big Lots filed for Chapter 11 on September 9, 2024, triggering a cascade of changes that altered every aspect of how the stock trades, what it represents, and what investors can realistically expect from it.

Chapter 11 is a form of bankruptcy restructuring that allows a company to reorganize its debts under court supervision while continuing operations. It does not mean immediate liquidation. However, for public shareholders, Chapter 11 is rarely a neutral event. In most cases, existing equity is severely diluted or rendered worthless as the reorganization process prioritizes secured creditors, bondholders, and other senior claimants above common stockholders.

When a stock enters this territory, several things happen quickly:

- Delisting from major exchanges: Big Lots shares were removed from their primary listing and now trade over-the-counter (OTC), reflected in the new ticker BIGGQ. The "Q" suffix is a well-recognized market signal that the company is in bankruptcy proceedings.

- Pricing disconnects: OTC bankruptcy stocks often see wild price swings driven by speculation, short squeezes, or retail investor sentiment rather than fundamental value.

- Suspension of normal reporting: Regular earnings calls and forward guidance become secondary to court filings, creditor negotiations, and restructuring updates.

- Valuation decoupled from operations: The company's actual retail performance becomes largely irrelevant to the stock's price trajectory.

"Understanding that Big Lots is no longer a typical retail investment is not pessimism; it is the prerequisite for making any rational decision about the security."

For investors who want to track similar restructuring cases or study their financial patterns, reviewing the GQG financial data on Tickerplace provides useful comparative context on how distressed equities behave during restructuring periods.

What 'BIGGQ' actually represents: Security mechanics post-bankruptcy

The ticker BIGGQ is not simply a renamed version of the old Big Lots stock. It is a fundamentally different type of security, and treating it otherwise is the most common and expensive mistake retail investors make in this situation.

When a company files for Chapter 11, its existing common equity becomes a subordinate claim in the bankruptcy estate. The valuation of BIGGQ is dominated by restructuring terms, including debtor-in-possession (DIP) financing arrangements, any asset sale process, and whether the reorganization converts to a liquidation. Standard discounted cash flow (DCF) analysis or price-to-earnings (P/E) multiples are simply not applicable here.

Here is what actually drives value in a post-bankruptcy security like BIGGQ:

- Claim seniority: Secured creditors get paid first; unsecured creditors second; equity holders last. Common shareholders almost never recover anything meaningful.

- DIP financing: This is new money lent to the company during bankruptcy to keep operations running. DIP lenders hold the most senior claim and are typically repaid before any other creditor.

- Sale vs. reorganization path: If assets are sold to a buyer (as occurred with Big Lots when Nexus Capital Management acquired the brand), equity value depends entirely on whether the sale proceeds exceed all senior claims.

- Liquidation value: In a full liquidation, assets are sold and distributed strictly by seniority. Equity is last in line and typically receives nothing.

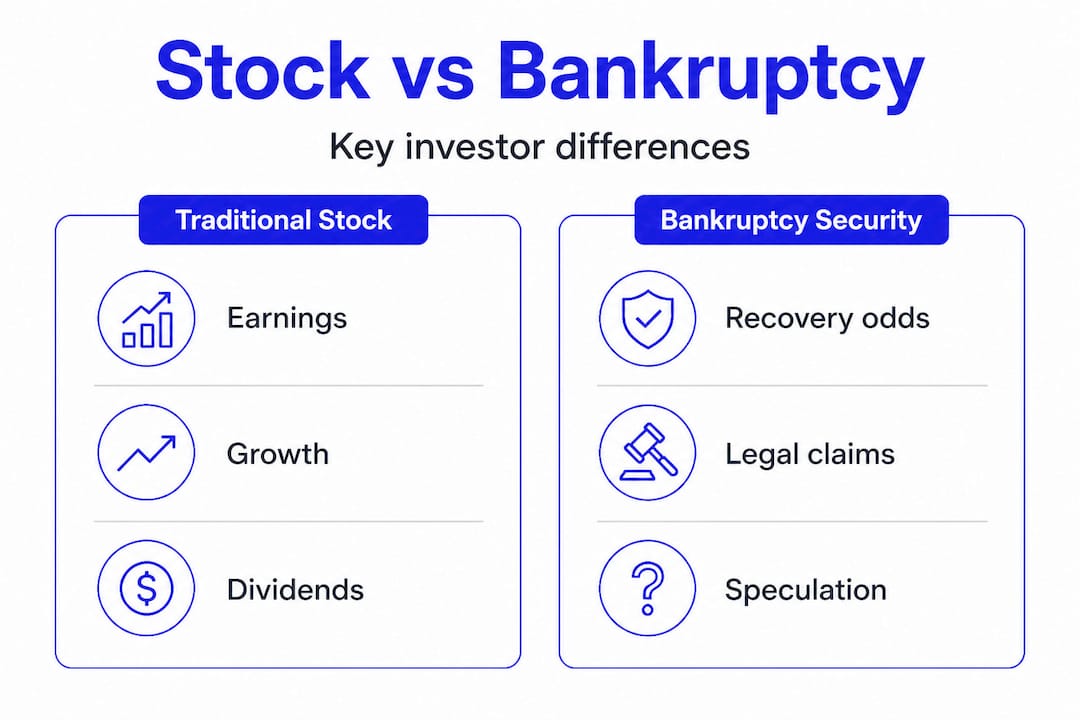

Comparison: Traditional stock vs. bankruptcy security

| Factor | Traditional stock | Bankruptcy security (BIGGQ) |

|---|---|---|

| Valuation driver | Earnings, growth, multiples | Recovery rates, claim hierarchy |

| Price transparency | High (exchange listed) | Low (OTC, speculative) |

| Information source | Earnings reports | Court dockets, filings |

| Investor protection | SEC regulated exchange | Limited OTC oversight |

| Recovery probability | Variable but defined | Low, often zero for equity |

Pro Tip: Before buying any OTC bankruptcy security, read the most recent court docket filing. This is publicly available through PACER (Public Access to Court Electronic Records) and contains the most current information about recovery prospects. Retail investors who skip this step are essentially trading blind.

For a broader view of how bankruptcy stock investing works across different cases, Tickerplace offers educational resources that can sharpen your analytical approach.

How to analyze and value Big Lots stock after bankruptcy

Distressed debt investors use a completely different playbook when evaluating securities like BIGGQ. The goal is not to find a mispriced growth stock. It is to estimate the probability and size of recovery for each class of claimant, then determine whether the current market price offers a genuine edge.

Standard tools like P/E ratios or revenue growth models carry no weight here. As the restructuring terms show, valuation is entirely driven by the DIP process, sale outcomes, and claim seniority rather than operating metrics.

Here is a practical step-by-step framework for evaluating a post-bankruptcy security:

- Identify total claims: Determine the total amount owed to all creditors, broken down by secured, unsecured, and subordinated tiers.

- Estimate asset value: What are the company's assets worth in a sale or liquidation? Court filings and any Section 363 sale documents are your primary sources.

- Map recovery by seniority: Work down the capital structure. How much do secured creditors recover? After that, is there anything left for unsecured creditors? After that, equity?

- Assess probability of reorganization vs. liquidation: A successful reorganization may preserve more value than a liquidation, but equity typically gets wiped out in both scenarios.

- Monitor court developments actively: New bids, DIP amendments, and creditor committee objections all shift the recovery calculus significantly.

- Assign probability weights to outcomes: Experienced distressed investors use scenario trees, assigning probabilities (e.g., 70% liquidation with zero equity recovery, 30% partial reorganization with minimal equity recovery).

Illustrative recovery scenario table

| Scenario | Probability | Secured creditor recovery | Equity recovery |

|---|---|---|---|

| Full liquidation | 60% | 80-90% | 0% |

| Asset sale (Section 363) | 30% | 90-100% | 0-2% |

| Successful reorganization | 10% | 100% | 1-5% |

You can explore bankruptcy stock examples and review delisted equity histories in the NYSE delisted stocks section to contextualize what these numbers look like historically.

Pro Tip: If the math above shows near-zero equity recovery in every realistic scenario, no price is cheap enough to justify buying the common stock on fundamental grounds. Speculation is a different activity than investing; know which one you are doing.

Lessons from other bankruptcy stocks and trading strategies

History is consistent on one point: most bankruptcy stocks eventually go to zero or near-zero for equity holders. The high-profile exceptions, where equity retained meaningful value, share specific conditions that are rarely present in large retail bankruptcies like Big Lots.

The restructuring dynamics that drive outcome distribution in cases like BIGGQ are well-documented across comparable situations, whether in retail, energy, or manufacturing bankruptcies.

Comparative bankruptcy stock outcomes

| Company | Filing year | Equity outcome | Key factor |

|---|---|---|---|

| Toys "R" Us | 2017 | Zero recovery | Liquidation, no reorganization |

| Sears Holdings | 2018 | Near-zero | Asset sale, equity wiped |

| J.Crew | 2020 | Minimal recovery | Debt-to-equity conversion |

| Hertz | 2020 | Partial recovery | Unique asset base, EV demand |

Hertz is the notable exception that retail traders often cite to justify speculation. But Hertz's partial equity recovery was driven by highly unusual circumstances: a sudden spike in used car values during the pandemic and an unprecedented DIP financing structure. These conditions are not transferable to a discount retailer.

Key risk management principles for trading BIGGQ or any bankruptcy security:

- Size positions as if the loss is 100%: Because it often is. Never allocate more than you can afford to lose entirely.

- Avoid averaging down: Adding to a losing position in a bankruptcy security usually magnifies losses, not recoveries.

- Watch for reverse splits or share cancellation: These can wipe positions without warning.

- Track institutional activity: If professional distressed investors are not buying equity, that is significant information.

You can review the MQG financials on Tickerplace as a comparative case study when evaluating market behavior around distressed securities.

Pro Tip: Volatility spikes in bankruptcy stocks are almost always speculative, not fundamental. A Reddit-driven price surge in BIGGQ does not change the legal priority structure one bit.

The uncomfortable truth about Big Lots stock (and most bankruptcy plays)

Here is what experienced distressed investors know that most retail traders ignore: the moment a company files Chapter 11, the common equity is functionally a lottery ticket, not a stock. The legal framework of bankruptcy, not market sentiment, determines outcomes.

Retail investors often buy BIGGQ because they remember Big Lots as a real, operating business. Nostalgia is not a valuation model. Reddit speculation about "turnaround potential" does not override a court-supervised priority waterfall. When you treat BIGGQ as a bankruptcy outcome security rather than a discounted version of the old Big Lots, the math becomes very clear very fast.

What makes this particularly dangerous is the price action. OTC bankruptcy stocks routinely trade at prices that imply irrational recovery expectations. A stock priced at $0.05 feels like a bargain, but $0.05 with a 98% chance of zero is not cheap.

The investors who profit from distressed situations are typically not buying equity at all. They buy secured debt at a discount, then influence the restructuring process to maximize recovery at their seniority level. Retail investors do not have access to that strategy. What retail investors have access to is speculative equity trading with asymmetric downside.

Understanding this reality is not discouraging. It is empowering. Recognizing when to stay out of a trade is one of the highest-value skills in investing, and it is one that advanced investing education can help you develop systematically.

Explore deeper bankruptcy investing tools and education

Navigating complex situations like Big Lots requires more than a basic stock screener. Tickerplace provides the analytical infrastructure to research distressed equities with precision.

With Tickerplace, you can access a powerful stock market research platform built for serious investors. Use the bankruptcy stock screener to filter and identify securities with specific risk profiles, or apply the debt to equity calculator to evaluate leverage levels before entering any position. Whether you are studying Big Lots or screening the broader market for distressed opportunities, Tickerplace gives you the data and tools to make decisions grounded in evidence rather than speculation.

Frequently asked questions

What does the BIGGQ ticker symbol mean for Big Lots stock?

BIGGQ is the post-bankruptcy ticker for Big Lots, signaling its status as an OTC bankruptcy security rather than a standard exchange-listed equity.

Can normal valuation methods still be used for Big Lots stock?

No. Standard models like P/E or DCF do not apply because valuation is driven by restructuring terms and claim seniority, not operating performance.

What risks do investors face holding BIGGQ?

Investors face the real possibility of total loss, since equity claims are subordinate to all creditors and bankruptcy outcomes rarely leave anything for common shareholders.

How long does bankruptcy restructuring typically affect the stock price?

Bankruptcy proceedings typically span months to over a year, with ongoing price volatility as court decisions, sale processes, and creditor negotiations produce new information throughout.