TL;DR:

- IAG remains operationally resilient, with underlying profits growing despite statutory declines caused by weather and litigation reserves.

- Recent share price volatility is driven primarily by legal risk perception, notably Greensill litigation concerns, rather than fundamental business weakness.

ASX IAG refers to Insurance Australia Group Limited, a leading general insurer listed on the Australian Securities Exchange under the ticker IAG. With a market cap near $18.2 billion and brands including NRMA, RACV, and CGU, IAG writes over $14 billion in premiums annually across Australia and New Zealand. For individual investors and market analysts, IAG represents one of the most significant non-bank financial stocks on the ASX. Recent share price volatility, driven by legal uncertainty rather than operational weakness, makes understanding the distinction between headline noise and underlying performance the defining challenge of any IAG stock analysis in 2026.

What has driven recent fluctuations in ASX IAG's share price?

The most direct answer: legal risk perception, not business deterioration, caused IAG's sharpest recent price moves. On May 22, 2026, IAG shares fell 4.54% to $7.78 after Citi downgraded the stock from "buy" to "neutral." That single-day drop reflected the market's reaction to Greensill Capital litigation exposure, not any change in IAG's insurance operations. The downgrade amplified existing investor anxiety, compressing the share price further within a 12-month period that already showed an 11% decline.

The Greensill litigation is the central concern. IAG provisioned $432 million for legal fees related to this exposure, a figure large enough to alarm the market even though the company asserts it expects no net liability. That gap between precautionary provisioning and actual expected loss is where investor sentiment diverges from management's stated position.

Key factors behind recent IAG share price volatility include:

- Citi downgrade from "buy" to "neutral" on May 22, 2026, citing Greensill litigation risk

- $432 million legal provision recorded as a precautionary measure despite no expected net exposure

- 11% share price decline over the 12 months preceding the downgrade

- Market sentiment amplifying legal uncertainty beyond what operational data justifies

Market analysts note that IAG's volatility is more a product of sentiment and legal uncertainty than underlying operational problems. That distinction matters enormously when you are deciding whether a price dip represents a buying opportunity or a genuine warning signal.

How is IAG's core insurance business performing?

IAG's underlying business tells a materially different story from its share price trajectory. In H1 2026, statutory net profit fell 35% due to a $174 million weather impact, a figure that sounds alarming until you separate it from the underlying insurance profit, which rose 7.6% to $804 million. The underlying insurance margin held steady at 15.1%, and management maintained full-year guidance. This is the metric that experienced analysts prioritize over statutory results.

Pro Tip: When evaluating IAG's results, always compare underlying insurance profit and margin against prior periods rather than focusing on statutory net profit. Weather events and litigation provisions distort the statutory figure significantly, making it a poor indicator of operational health.

The premium growth picture reinforces this view. IAG forecasts high single-digit premium growth for FY2026, with the Australian retail segment already delivering 14.4% top-line growth in H1 2026. Full-year insurance profit guidance sits between $1.55 billion and $1.75 billion.

| Metric | H1 2026 Result |

|---|---|

| Statutory net profit change | Down 35% (weather impact: $174M) |

| Underlying insurance profit | $804M, up 7.6% year on year |

| Underlying insurance margin | 15.1% |

| Australian retail premium growth | 14.4% |

| FY2026 insurance profit guidance | $1.55B to $1.75B |

The contrast between statutory and underlying results is not an accounting trick. IAG's share price is highly sensitive to catastrophic weather events and litigation reserve changes, both of which can obscure a fundamentally sound operating business. Investors who read only the headline profit figure will consistently misread IAG's performance.

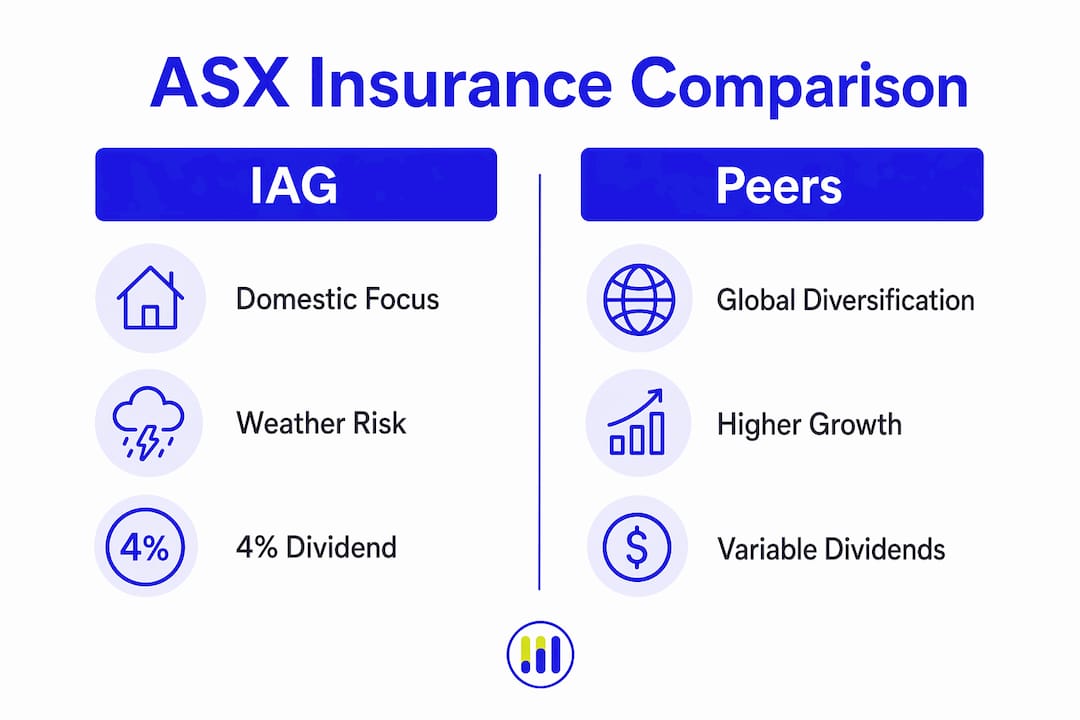

How does IAG compare to other ASX insurance companies?

Positioning IAG within the broader ASX insurance sector reveals both its strengths and its relative underperformance in recent years. In 2025, Medibank rose nearly 26% while IAG fell over 7%. QBE led the sector with strong diversified global exposure, while Suncorp dropped approximately 22%, partly due to its own structural changes following the sale of its banking division.

| Company | 2025 Share Performance | Key Differentiator |

|---|---|---|

| IAG | Down ~7% | Domestic focus; weather and litigation exposure |

| Medibank | Up ~26% | Health insurance; lower catastrophe risk |

| QBE | Sector leader | Global diversification; commercial lines |

| Suncorp | Down ~22% | Post-bank sale restructuring underway |

The comparison highlights a structural reality: IAG's concentration in Australian general insurance makes it more exposed to domestic weather events than QBE's globally diversified book. Medibank operates in health insurance, a different risk profile entirely, which explains its stronger 2025 performance. For investors building a position in ASX-listed insurers, understanding these distinctions prevents false equivalence between companies that share a sector label but carry very different risk profiles.

IAG's dividend yield near 4% and P/E ratio near 17 position it as a mid-range value proposition among ASX insurance companies. Rising premiums combined with disciplined underwriting make IAG attractive relative to traditional big-four banks, particularly for income-focused investors seeking exposure outside the banking sector.

What are the key risks and opportunities for ASX IAG investors?

The risk and opportunity profile for IAG in 2026 is unusually asymmetric. The primary risk is legal, not operational. The $432 million Greensill provision represents a significant precautionary reserve despite management's assertion of no expected net exposure. If litigation outcomes exceed provisions, the financial impact on earnings could be material. If the exposure resolves favorably, the provision reversal would provide a meaningful earnings uplift.

Key risks for IAG investors:

- Greensill litigation outcome uncertainty despite $432 million provision

- Catastrophic weather events that inflate claims and suppress statutory profit

- Integration costs from business consolidation affecting near-term margins

- Analyst sentiment shifts that can move the share price independent of fundamentals

Key opportunities for IAG investors:

- Premium growth of high single digits forecast for FY2026, driven by pricing discipline

- $200 million share buyback program signaling management confidence in capital strength

- Underlying margin stability at 15.1%, demonstrating operational resilience

- Potential litigation provision reversal if Greensill exposure resolves below provisioned amounts

Pro Tip: Track IAG's financial statements each reporting period with a focus on the underlying insurance margin and net earned premium growth. These two metrics will tell you more about IAG's trajectory than any single statutory profit figure.

The share buyback of up to $200 million is a concrete signal. Management does not authorize buybacks when they believe the capital base is under pressure. That decision, made alongside maintained full-year guidance, suggests the board views current share prices as undervalued relative to intrinsic worth.

Key Takeaways

IAG's underlying insurance business remains operationally sound in 2026, with legal uncertainty and weather events distorting the statutory profit picture far more than any structural business weakness.

| Point | Details |

|---|---|

| Legal risk is the primary driver | The $432M Greensill provision, not operations, caused the May 2026 share price drop. |

| Underlying profit tells the real story | Underlying insurance profit rose 7.6% to $804M in H1 2026 despite a 35% statutory decline. |

| Premium growth supports the outlook | IAG forecasts high single-digit premium growth for FY2026 with 14.4% retail growth already recorded. |

| Sector comparison favors selectivity | IAG underperformed Medibank and QBE in 2025; risk profile differs significantly across ASX insurers. |

| Buyback signals management confidence | A $200M on-market share buyback reflects a strong capital position and shareholder return focus. |

Tickerplace's read on IAG: separating signal from noise

The most common mistake investors make with IAG is treating statutory net profit as the primary performance indicator. It is not. Weather events and litigation provisions are real costs, but they are also transient and often non-recurring. The underlying insurance margin at 15.1% and premium growth above 14% in the Australian retail segment are the numbers that define whether IAG's business model is working. Those numbers say it is.

The Greensill litigation creates genuine uncertainty, and that uncertainty deserves respect. A $432 million provision is not trivial. But IAG's management has maintained full-year guidance and authorized a $200 million buyback in the same reporting period. Those are not the actions of a leadership team that believes the business is structurally impaired.

What concerns me more than the litigation itself is how quickly sentiment can move a stock like IAG when a major analyst firm changes its rating. The Citi downgrade on May 22, 2026, produced a 4.54% single-day decline on no new operational information. That kind of price sensitivity to analyst opinion, rather than earnings data, creates both risk and opportunity. If you are monitoring IAG's historical share price through 2026, watch for the litigation resolution timeline as the most likely catalyst for a re-rating in either direction.

The IAG share price forecast for the remainder of 2026 depends heavily on two variables: weather event frequency and Greensill litigation progress. Neither is predictable with precision. What is predictable is that IAG's core insurance business, measured by underlying profit and premium trends, continues to perform within the range management has guided. That consistency is worth something, even when the headline numbers obscure it.

— Tickerplace

Research and analyze ASX IAG with Tickerplace

Tickerplace gives you the tools to cut through the noise on stocks like IAG and build a clear, data-driven view of what you are actually buying. The Tickerplace stock screener lets you filter ASX insurance companies by margin, premium growth, dividend yield, and P/E ratio so you can compare IAG against QBE, Suncorp, and Medibank on the metrics that matter. The platform also provides access to financial statements, historical price data, and technical analysis for IAG and hundreds of other ASX-listed stocks. Whether you are evaluating IAG's underlying insurance margin or modeling the impact of a litigation provision reversal, Tickerplace delivers the data you need in one place. Start your research at Tickerplace today.

FAQ

What does ASX IAG stand for?

ASX IAG is the ticker symbol for Insurance Australia Group Limited on the Australian Securities Exchange. It should not be confused with International Airlines Group, which trades under the same ticker on the London Stock Exchange and NYSE.

Why did IAG's share price drop in May 2026?

IAG shares fell 4.54% on May 22, 2026, after Citi downgraded the stock from "buy" to "neutral" due to concerns about Greensill Capital litigation exposure and a $432 million legal provision.

What is IAG's insurance profit guidance for FY2026?

IAG's management has guided full-year insurance profit of between $1.55 billion and $1.75 billion for FY2026, supported by high single-digit premium growth and a stable underlying insurance margin of 15.1%.

How does IAG compare to other ASX insurance stocks?

In 2025, IAG fell over 7% while Medibank rose nearly 26% and QBE led the sector through global diversification. IAG's domestic concentration makes it more exposed to Australian weather events than its major ASX insurance peers.

Is the IAG share buyback a positive signal for investors?

IAG's $200 million on-market share buyback signals management confidence in the company's capital position. Buyback programs of this scale are generally interpreted as a sign that leadership views the current share price as undervalued relative to the business's underlying worth.