TL;DR:

- Tesla stock appears overvalued based on standard valuation models and 2026 market data. Its high price mainly reflects speculative growth expectations in autonomous driving, robotics, and AI instead of current earnings.

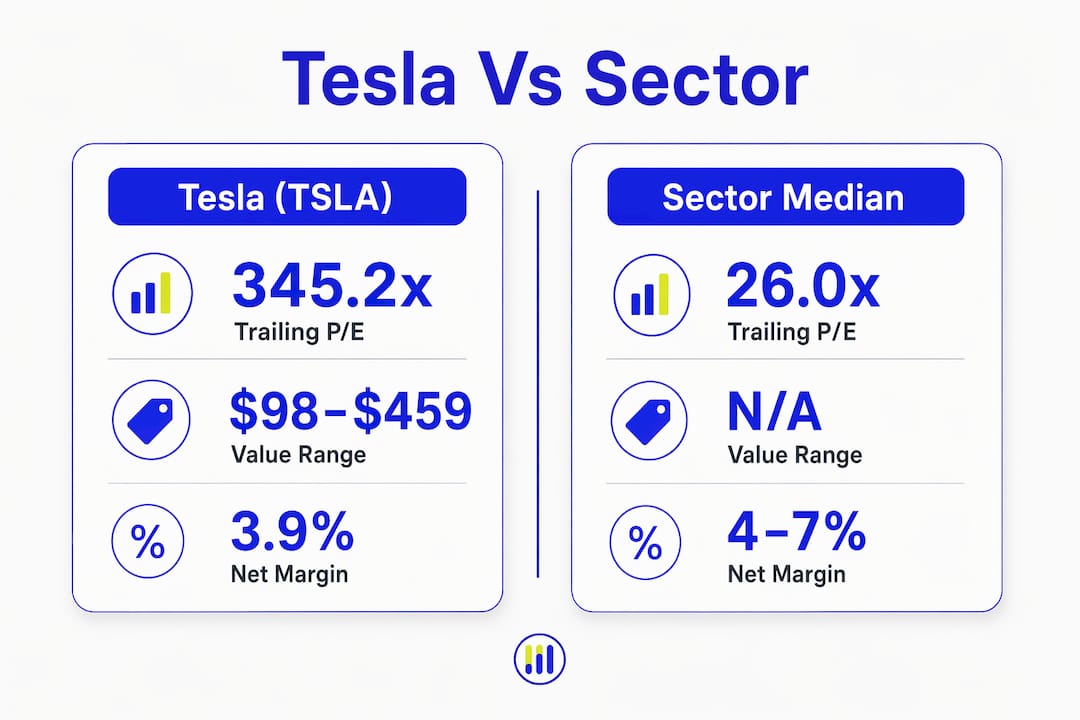

Tesla stock is currently overvalued relative to its intrinsic value, based on standard financial valuation models and 2026 market data. TSLA trades at a trailing P/E of 345.2x, a 1,228% premium to the sector median of 26x. That gap is not a rounding error. It reflects a market pricing in decades of speculative growth in autonomous driving, robotics, and artificial intelligence, all of which remain commercially unproven at scale. Understanding whether TSLA is undervalued or overvalued requires separating what Tesla earns today from what investors believe it will earn tomorrow.

Is TSLA undervalued or overvalued? What the models say

Quantitative valuation models produce a wide spread for Tesla's fair value. Intrinsic value estimates range from $98 to $459 per share, with an average 12-month analyst price target near $423. That range is not a sign of analytical incompetence. It reflects genuine uncertainty about Tesla's terminal growth rate, the single variable that drives the largest portion of any discounted cash flow (DCF) model output.

Analyst price targets show a similar spread. The consensus 12-month target sits around $421, but individual estimates run from $123 on the low end to $600 on the high end. A $477 spread between the most bearish and most bullish analysts tells you that TSLA financial evaluation is not a math problem with one answer. It is a judgment call about which future Tesla you believe in.

The table below summarizes key valuation metrics for TSLA against sector benchmarks.

| Metric | TSLA | Sector median |

|---|---|---|

| Trailing P/E | 345.2x | 26.0x |

| Intrinsic value range | $98–$459 | N/A |

| Average analyst price target | ~$421 | N/A |

| Market capitalization | $1.43 trillion | N/A |

Tesla's market capitalization of $1.43 trillion places it among the most valuable companies on earth. That valuation only makes sense if Tesla successfully commercializes businesses that do not yet generate meaningful revenue.

Key valuation signals investors should track:

- P/E ratio: Tesla's trailing P/E of 345.2x dwarfs automotive peers and most technology companies.

- PEG ratio: A high P/E paired with slowing revenue growth produces an unfavorable price-to-earnings-growth ratio.

- EV/EBITDA: Tesla's enterprise value relative to earnings before interest, taxes, depreciation, and amortization remains elevated compared to traditional automakers.

- DCF terminal value sensitivity: Small changes in the assumed long-term growth rate produce enormous swings in fair value output.

Why does TSLA's price depend so heavily on AI and robotics?

Tesla's stock price is not primarily a bet on car sales. It is a bet on terminal value, the estimated worth of all cash flows beyond the explicit forecast period. Terminal value accounts for 60–80% of intrinsic value in most DCF models applied to high-growth companies. For Tesla, that terminal value is almost entirely driven by assumptions about autonomous driving revenue, the Optimus humanoid robot, and AI-powered services.

The problem is that none of these businesses currently produce predictable cash flows. Tesla's valuation depends heavily on speculative long-term narratives that lack the revenue history needed to anchor a reliable model. When the core of your valuation sits in a speculative future, small changes in assumptions produce dramatic price swings.

Delays in products like Cybercab and Optimus can trigger rapid stock revaluations. Investors pricing in 2028 robotaxi revenue today will reprice sharply if that launch slips to 2030. This is not a hypothetical risk. It is the structural reason TSLA moves violently on product timeline news.

Pro Tip: Avoid using historical P/E ratios as your primary benchmark for Tesla. Because Tesla's business model is evolving rapidly, its historical earnings base is not a reliable anchor. Scenario-based analysis that assigns probabilities to different growth outcomes gives you a far more honest picture of fair value.

How do Tesla's near-term fundamentals affect its valuation?

Tesla's current financial results do not support its current stock price on their own. Net margin sits at 3.9% with revenue growth slowing, a combination that would make any traditional automaker look expensive at a fraction of Tesla's multiple. Margin pressure from price cuts, rising competition, and softening EV demand in key markets has compressed near-term profitability.

The competitive picture has changed materially. EV manufacturers across Asia and Europe have closed the technology gap that once gave Tesla a clear pricing advantage. As market share pressure builds, Tesla's ability to sustain premium pricing weakens, which directly reduces near-term earnings power.

The table below compares Tesla's financial profile against a typical automotive peer.

| Financial ratio | Tesla (TSLA) | Typical automotive peer |

|---|---|---|

| Net margin | 3.9% | 4–7% |

| Trailing P/E | 345.2x | 8–15x |

| Revenue growth trend | Slowing | Stable to moderate |

| Valuation basis | Speculative growth | Current earnings |

The gap between Tesla's multiple and a typical automotive peer's multiple is not explained by current fundamentals. It is explained entirely by future expectations. That distinction matters when you assess Tesla's market value against what the business actually earns today.

What practical approaches help investors evaluate TSLA's fair value?

The most rigorous framework for Tesla stock analysis is a probability-weighted scenario model, a method that assigns different likelihoods to bull, base, and bear cases rather than relying on a single point estimate. This approach, advocated by analysts including Anton Ladnyi, CFA, acknowledges that the correct valuation framework is a probability distribution, not a single number. It forces you to be explicit about your assumptions and honest about your uncertainty.

Margin of safety is equally important. Buying a stock at or above the midpoint of a wide intrinsic value range leaves no buffer for error. For Tesla, where the range spans from $98 to $459, the margin of safety calculation is not academic. It is the difference between a disciplined investment and a speculative bet.

Investors conducting a serious TSLA investment review should monitor the following factors:

- Cybercab and Semi launch timelines: Delays directly reduce the present value of future autonomous revenue.

- Optimus robot commercialization: Any credible revenue signal from Optimus would materially shift bull-case valuations.

- Automotive gross margin trends: Recovering margins would reduce the gap between current earnings and the stock's implied value.

- Regulatory progress on full self-driving: Approval timelines in the US and Europe determine when autonomous revenue can realistically begin.

- Competitive market share data: Quarterly delivery figures relative to global EV market growth reveal whether Tesla is gaining or losing ground.

Using a stock valuation calculator that incorporates both P/E and DCF inputs lets you test how sensitive your fair value estimate is to each of these variables. Running your own numbers with different growth rate assumptions is more informative than accepting any single analyst's target.

Key Takeaways

Tesla is currently overvalued relative to its intrinsic value under most standard models, with its premium price reflecting speculative growth assumptions in AI, robotics, and autonomous driving rather than current earnings.

| Point | Details |

|---|---|

| Extreme valuation premium | Tesla's trailing P/E of 345.2x is 1,228% above the sector median of 26x. |

| Wide intrinsic value range | DCF models produce a $98–$459 per share range, signaling high uncertainty. |

| Speculative growth dependency | Terminal value drives 60–80% of Tesla's modeled intrinsic value. |

| Near-term fundamentals are weak | A 3.9% net margin and slowing revenue growth do not justify the current multiple alone. |

| Use scenario-based valuation | Probability-weighted models give a more honest fair value than single-point estimates. |

Tickerplace's take on valuing Tesla in 2026

Tesla is one of the most genuinely difficult stocks to value, and that difficulty is not a flaw in the analysis. It is the correct conclusion. The $98 to $459 intrinsic value range is not a failure of financial modeling. It is an honest representation of how uncertain Tesla's future actually is.

What concerns us is not that Tesla might be worth $459. It might be. What concerns us is that investors often treat the bull case as the base case, pricing in full execution of autonomous driving, robotics, and AI services without adequately weighting the probability of delays, competition, or regulatory friction. The TSLA price prediction debate is really a debate about which scenario deserves the most weight.

Disciplined investors should hold a position size in TSLA that reflects genuine uncertainty, not conviction. Revisit your valuation assumptions every quarter as new product and margin data arrives. Tesla's story is still being written, and the market's current chapter may not be the final one.

— Tickerplace

Tickerplace tools for your TSLA valuation analysis

Determining whether TSLA is a buy requires more than reading analyst reports. It requires running your own numbers against your own assumptions.

Tickerplace provides free, institutional-grade tools built for exactly this kind of analysis. The stock valuation calculator lets you model Tesla's fair value using P/E and intrinsic value inputs, so you can test how sensitive your conclusion is to different growth rate assumptions. The stock valuation checker gives you an instant overvalued or undervalued signal across multiple models, updated daily. For investors who want to go deeper, the intrinsic value calculator walks you through a full DCF analysis with your own inputs. All tools are free, with no subscription required.

FAQ

Is TSLA currently overvalued?

Tesla is overvalued relative to its current earnings, trading at a trailing P/E of 345.2x versus a sector median of 26x. Its price reflects speculative future growth, not present financial performance.

What is Tesla's intrinsic value per share?

Intrinsic value models produce a range of $98 to $459 per share for Tesla, with an average 12-month analyst price target near $421. The wide range reflects deep uncertainty about Tesla's long-term growth in AI and autonomous driving.

Why do analyst price targets for TSLA vary so much?

Analyst targets for TSLA range from $123 to $600 because Tesla's valuation is highly sensitive to assumptions about terminal growth in robotics and autonomous driving. Small changes in those assumptions produce large swings in fair value.

Is Tesla a good investment at current prices?

Whether Tesla is a good investment depends on your confidence in its autonomous driving and robotics timelines. At current prices, the margin of safety is thin, and near-term fundamentals including a 3.9% net margin do not support the valuation independently.

What is the best way to value TSLA stock?

A probability-weighted scenario model is the most reliable approach for Tesla stock analysis. Assign realistic probabilities to bull, base, and bear cases, then weight the resulting fair values rather than relying on a single DCF output.