TL;DR:

- Despite strong H1 earnings and robust capital ratios, ANZ's share price declined due to market concerns about interest rate hikes and margin compression. Investors should consider macroeconomic factors, dividend franking, and valuation ratios to assess its true value and future prospects. Patience and comprehensive analysis remain essential for capitalizing on price-earnings disconnects in banking stocks.

ANZ Bank's share price has presented investors with a genuine puzzle in 2026. The bank posted a 14% cash profit rise in H1, raised its interim dividend, and strengthened its capital position. Yet the ANZ bank share price moved lower year-to-date. For investors accustomed to equating strong earnings with rising stock prices, this disconnect demands a clear explanation. This article works through the financial results, market dynamics, and macroeconomic forces shaping ANZ's current valuation so you can assess the stock with confidence.

Key Takeaways

| Point | Details |

|---|---|

| Strong financial results | ANZ reported a 14% increase in cash profit for H1 2026, demonstrating underlying business strength. |

| Share price lag | Despite profits, ANZ shares fell 2.22% year-to-date due to macroeconomic concerns. |

| Macroeconomic influence | Rate hike expectations and inflation risks heavily impact ANZ’s share valuation. |

| Stable dividends | ANZ maintains an 83 cent dividend with increased franking, supporting income investors. |

| Investor strategy | Analyzing both financial metrics and economic trends is essential for informed decisions. |

Understanding ANZ's recent financial performance

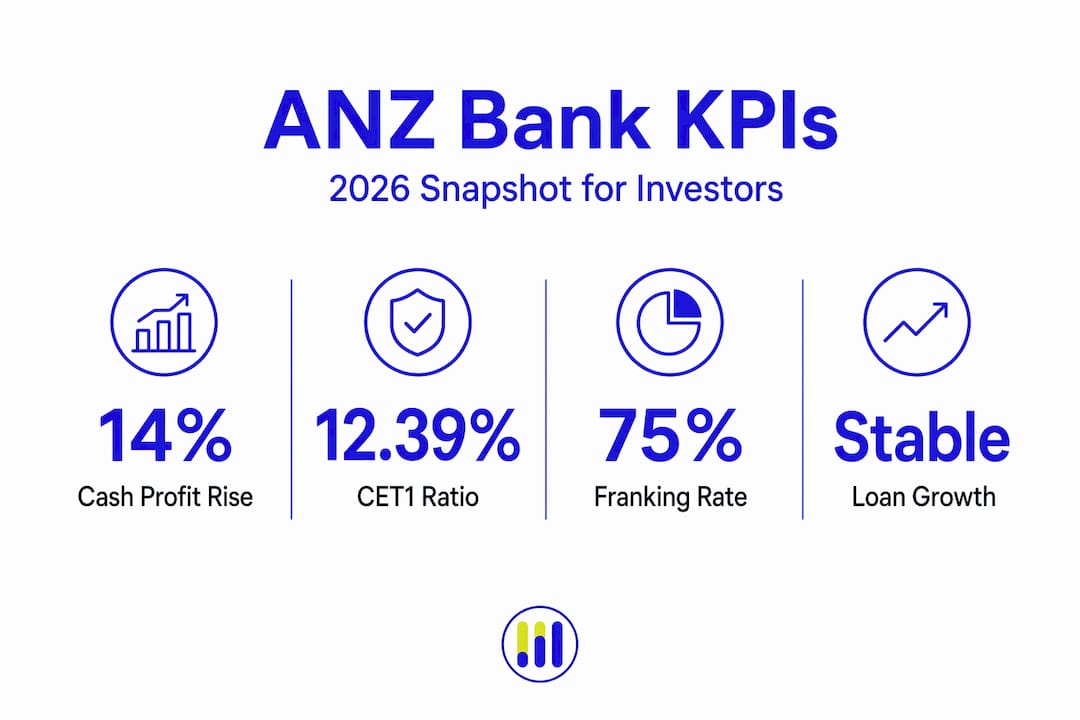

ANZ's H1 2026 results were, by most measures, genuinely solid. The bank reported a cash profit of A$3.78 billion for the half year ended 31 March 2026, up 14% from the prior half excluding significant items. Statutory profit held steady at A$3.65 billion. These are not marginal improvements; they reflect meaningful earnings momentum that most major banks in the region would welcome.

"For the half year ended 31 March 2026, ANZ proposed an interim dividend of 83 cents per share, 75% franked, up from 70% in the prior period, signaling management's confidence in capital sustainability."

Key metrics from the H1 2026 report include:

- Cash profit: A$3.78 billion, up 14% excluding significant items

- Statutory profit: A$3.65 billion

- Interim dividend: 83 cents per share, 75% franked

- CET1 ratio (Common Equity Tier 1): 12.39%, up 36 basis points from September 2025

- Cost-to-income ratio: 49.4%

What stands out, beyond the headline figures, is the loan and deposit growth dynamic. Customer deposits grew at a faster pace than net loans and advances, which creates a structural tension in how the bank generates net interest margin (NIM), the spread between what it earns on loans and pays on deposits. Review ANZ's detailed ANZ financial statements to track how this balance evolves across reporting periods.

Why ANZ's strong profit did not lift its share price

Here is where many investors get tripped up: earnings and share price are not the same signal. They respond to different inputs, on different timescales, and with very different sensitivities to macro conditions.

The current ANZ share price reflects investor anxiety that runs ahead of reported results. By May 2026, shares were down 2.22% year-to-date despite the strong H1 earnings, driven primarily by renewed concerns about Reserve Bank of Australia (RBA) rate hike probabilities running at roughly 70%. When markets price in higher interest rates, they often reprice bank stocks lower, even profitable ones.

Why? A few interconnected reasons:

- Net interest margin compression: If deposit rates rise faster than lending rates, the spread narrows, and future earnings look less impressive than current ones.

- Loan demand sensitivity: Higher rates slow borrowing activity, moderating ANZ's growth runway.

- Valuation recalibration: Investors discount future earnings more steeply in a higher-rate environment, reducing present-value multiples.

- Market sentiment timing: Stock prices respond to forward expectations, not backward-looking profit reports.

"The market is always pricing tomorrow, not yesterday. A strong earnings report tells you what happened; the share price tells you what investors think will happen next."

Pro Tip: When evaluating ANZ bank shares price movements around earnings releases, check the RBA rate futures curve alongside the profit figures. If rate hike probability spikes in the same week as a results announcement, even strong earnings can fail to lift the stock. Read more on ANZ share price insights to understand how these dynamics interact in real time.

Analyzing ANZ's key financial ratios and market valuation

Numbers tell a more nuanced story than headlines. ANZ's fundamentals place it firmly in the category of well-capitalized, income-generating banks, and understanding the ratios helps you assess whether the current price represents fair value, a discount, or a risk premium.

| Metric | ANZ H1 2026 value | What it signals |

|---|---|---|

| CET1 ratio | 12.39% | Strong capital buffer above regulatory minimums |

| Cost-to-income ratio | 49.4% | Competitive operational efficiency |

| Dividend yield | ~4.44% | Reliable income stream for investors |

| Dividend franking | 75% | Enhanced after-tax returns for Australian investors |

| Beta | ~0.57 | Lower volatility relative to the broader market |

The CET1 ratio of 12.39% comfortably exceeds the Australian Prudential Regulation Authority (APRA) requirements, which means ANZ carries a healthy cushion against credit losses or economic stress. That matters when evaluating downside risk in the ANZ bank share price ASX context.

The dividend yield of approximately 4.44% is not trivial. With 75% franking, the grossed-up yield is materially higher for Australian tax-resident investors who can claim the franking credits. This supports the stock's floor in periods of price weakness.

- Low beta of ~0.57 means ANZ tends to move less than the broader index, making it a relatively defensive holding.

- Cost-to-income near 50% is broadly competitive among major Australian banks; improvements here would be a positive catalyst.

- Valuation discounts at the sector level often reflect macro risks more than company-specific deterioration.

Pro Tip: Compare ANZ's ratios against peers using a bank valuation comparison tool. ASX share prices for CBA and other major banks often move in correlated patterns during macro events, which can help you identify whether a move in ANZ is bank-specific or sector-wide. Track updated figures through ANZ financial data.

Implications of macroeconomic factors on ANZ's share price outlook

After ANZ's H1 results were released, the share price dropped 2-3% as markets quickly pivoted to concerns about margin compression and the sustainability of earnings in a higher-rate environment. This reaction is instructive. It shows that ANZ bank market trends are increasingly shaped by forces outside the bank's direct control.

The core macroeconomic factors to watch:

- RBA rate decisions: Each rate move alters the funding cost environment and borrowing demand simultaneously.

- Inflation trajectory: Persistent inflation means higher costs for ANZ operationally and raises credit risk among borrowers.

- Deposit vs. loan growth gap: When deposits outpace lending, as they did in H1 2026, banks face pressure deploying capital at competitive returns.

- Competitive lending environment: Major banks are competing aggressively on mortgage pricing, squeezing margins from the asset side.

- Economic cycle risks: A slowing economy reduces credit demand and raises default probabilities, both headwinds for ANZ's earnings outlook.

"Deposit growth outpacing loan growth is not just an accounting observation. It signals that households are saving more than borrowing, which has direct implications for how ANZ deploys its balance sheet and manages profitability."

Understanding these dynamics is essential to forming a view on the ANZ share price market factors that will define its next directional move.

Key strategies for investors analyzing ANZ share price trends

Applying the analysis above to actual investment decisions requires a structured approach. ANZ's situation in 2026 is a textbook case for why banking stocks reward investors who go beyond the earnings headline.

ANZ CEO commentary highlighted stable margins amid intense competition, which underscores that margin management will be the defining variable for earnings sustainability in coming halves.

Here is a practical framework for investors tracking the ANZ bank share price ASX listing:

- Monitor RBA meeting outcomes closely. Rate changes move bank sector valuations quickly and often override earnings signals.

- Track both lending and deposit growth rates separately. A widening gap between the two signals future NIM pressure that profits may not yet reflect.

- Assess dividend sustainability, not just yield. A 4.44% yield is attractive, but verify payout ratios and franking levels remain supportable by earnings.

- Watch sector correlations. ASX CBA and ANZ often move together during macro-driven sell-offs; distinguishing sector risk from company risk matters.

- Use real-time data for entry and exit timing. ANZ share price history shows that patience around macro events can improve entry points meaningfully.

Pro Tip: If you are income-focused, prioritize the grossed-up dividend yield (accounting for franking credits) rather than the nominal yield. For investors in the 30% tax bracket or above, the franking adjustment can add 1-2 percentage points to your effective return. Explore stock investing education resources to build your understanding of dividend mechanics and portfolio positioning.

Why the ANZ share price paradox reflects deeper market realities

Most investors instinctively expect a straight line between profits and price. ANZ in 2026 proves that line bends, sometimes sharply, under the weight of macro expectations, rate cycles, and market sentiment.

The more important observation is this: ANZ's situation is not exceptional. It is the norm for mature banking stocks in rate-sensitive markets. Profits are reported quarterly. Interest rate expectations reprice daily. The stock market is always running ahead of the balance sheet. When those two timelines collide, as they did after ANZ's H1 release, the result looks like a paradox but it is actually the market doing exactly what it is designed to do.

What experienced investors recognize, and newer investors often miss, is that periods of share price weakness disconnected from earnings fundamentals can present genuine value opportunities. ANZ's defensive characteristics, its low beta, its franked dividend, its well-capitalized balance sheet, do not disappear because the RBA raised rates. They become more relevant, not less, when uncertainty rises.

The dividend franking improvement from 70% to 75% received almost no attention in mainstream coverage, yet for long-term Australian investors it represents a measurable enhancement in total after-tax shareholder return. Overlooked details like that often separate investors who generate consistent returns from those who chase headlines.

Patience and holistic analysis are not passive virtues in banking stock investing. They are active edges. Track ANZ's evolving picture with ANZ share price analysis tools that connect financial data to market context in one place.

Explore ANZ stock insights and tools on Tickerplace

Understanding the gap between ANZ's earnings strength and its share price movement is exactly the kind of analysis that separates informed investors from reactive ones.

Tickerplace gives you the data infrastructure to do this analysis consistently. Access up-to-date ANZ financial statements including earnings, capital ratios, and dividend history in one place. Use the platform's stock screener to compare ANZ against other major ASX-listed banks on key metrics like NIM, CET1, yield, and valuation multiples. And if you want to sharpen your fundamental analysis skills, the investing education section covers everything from dividend mechanics to how interest rate cycles affect bank valuations. Good decisions start with complete information.

Frequently asked questions

Why did ANZ's share price fall despite strong half-year profits?

ANZ's share price declined because investors shifted focus to RBA rate hike risks with a 70% probability of hikes, creating margin compression concerns that outweighed the positive earnings report.

What is the significance of ANZ's CET1 ratio for investors?

The CET1 ratio measures ANZ's core capital adequacy; at 12.39% in H1 2026, it signals strong financial stability and capacity to absorb economic shocks without endangering dividends or solvency.

How does the dividend franking rate affect ANZ's share attractiveness?

ANZ's franking rate rose from 70% to 75%, which increases the tax credits attached to each dividend payment, directly improving after-tax returns for Australian resident investors and making the stock more appealing for income-focused portfolios.

What macroeconomic factors should investors watch regarding ANZ's future share price?

Investors should track RBA interest rate decisions, inflation data, and the gap between deposit and loan growth, as these drive margin pressure and earnings sustainability more directly than headline profit figures.

Is ANZ considered a defensive or growth stock?

ANZ is positioned as a defensive banking stock, with a dividend yield of 4.44% and a low beta of 0.57, making it more suitable for investors seeking stable income and lower portfolio volatility than those pursuing aggressive capital growth.